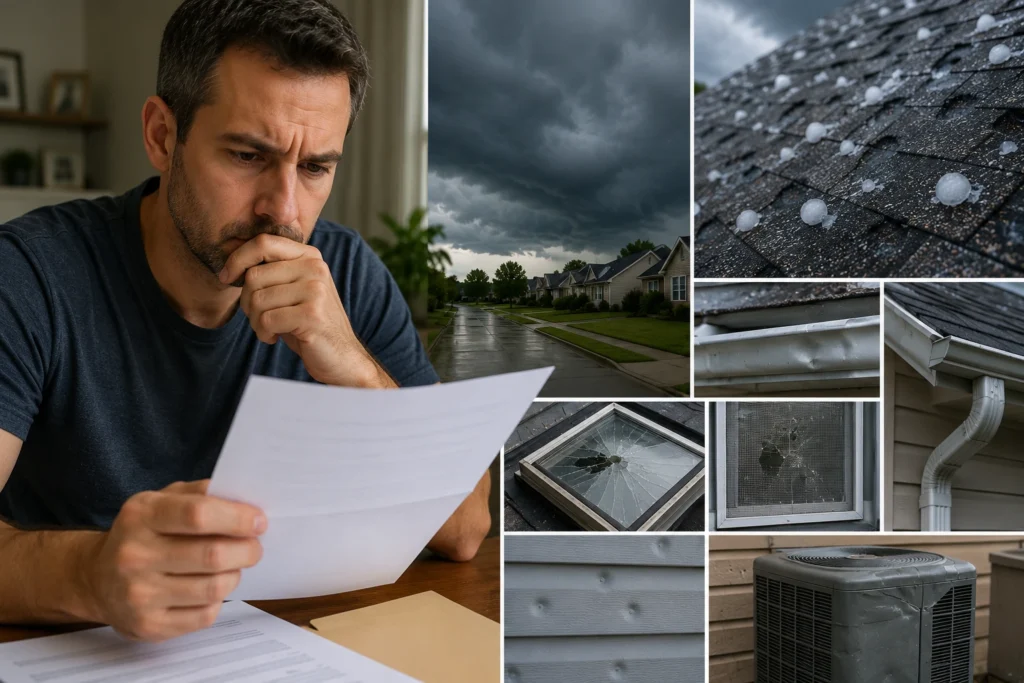

Few things frustrate homeowners more than discovering storm damage, filing an insurance claim, and then receiving a denial letter. Unfortunately, this scenario plays out every year across North Texas. Severe hailstorms regularly impact homes throughout Richardson, leaving behind damaged roofing systems, dented gutters, compromised siding, and water intrusion issues. Many homeowners assume their insurance policy will automatically cover the damage. Then the denial arrives.

If you’re searching for What to Do If Your Hail Claim Was Denied in Richardson, TX, you’re not alone. A denied claim can feel overwhelming. It can also leave property owners wondering whether they have any options left. The good news? A denial is not necessarily the end of the story.

Insurance claim decisions can be challenged. Additional evidence can be submitted. Inspections can be revisited. In some cases, denied claims are ultimately approved after further review. This guide explains exactly what homeowners should do after receiving a hail claim denial and how to improve the chances of obtaining a fair outcome.

Understanding Why Hail Claims Get Denied

Before challenging a denial, it’s important to understand why it happened. Insurance companies deny hail claims for many different reasons. Some denials are legitimate. Others may be based on incomplete inspections, missing documentation, or disagreements regarding the cause of damage.

Common Reasons Insurance Companies Deny Hail Claims

The most common reasons include:

- Alleged wear and tear

- Roof aging

- Maintenance-related issues

- Lack of visible hail impacts

- Missed reporting deadlines

- Disputed storm dates

- Previous unrepaired damage

- Policy exclusions

In many situations, insurers argue that the observed damage resulted from age rather than hail. This distinction often becomes the central issue in a dispute.

Partial Denials vs. Complete Denials

Not every denial rejects the entire claim. Some claims receive partial approval. For example, an insurer may approve gutter repairs but deny roof replacement. They may pay for minor repairs while rejecting more significant portions of the loss. In these situations, homeowners often face the same financial challenges as a full denial.

Reviewing the Denial Letter Carefully

The denial letter contains critical information. Do not skim it. Read every section carefully.

Pay particular attention to:

| Item | Why It Matters |

|---|---|

| Reason for denial | Identifies dispute points |

| Policy citations | References coverage language |

| Inspection findings | Shows insurer’s conclusions |

| Damage descriptions | Reveals overlooked issues |

| Appeal instructions | Explains next steps |

Many homeowners discover important clues within the denial letter itself.

Why Hail Claims Are Frequently Disputed in Richardson, TX

Richardson sits in a region known for severe weather. Spring and early summer storms routinely produce hail capable of causing substantial property damage. However, hail damage isn’t always obvious. That’s where disputes begin.

North Texas Hail Exposure

Richardson homeowners face repeated storm activity throughout the year.

Large hail can damage:

- Asphalt shingles

- Metal roofing

- Gutters

- Downspouts

- Skylights

- Window screens

- Siding

- HVAC equipment

Despite these risks, identifying storm-related damage sometimes becomes complicated.

Functional Damage vs. Cosmetic Damage

Many claim disputes revolve around a simple question: Does the damage affect function? Insurance companies often distinguish between cosmetic damage and functional damage.

Functional damage may impact:

- Water resistance

- Structural integrity

- Roof lifespan

- Manufacturer warranties

When homeowners and insurers disagree about this distinction, claim disputes frequently follow.

Challenges With Older Roofs

Roof age creates additional complications.

Insurers sometimes argue that:

- Cracking resulted from aging

- Granule loss occurred naturally

- Shingles deteriorated over time

- Repairs are sufficient instead of replacement

Independent evaluations often become essential in these situations.

Step 1: Review Your Denial Letter Line by Line

One of the biggest mistakes homeowners make is immediately assuming the insurance company’s decision is final. Instead, slow down. Study the denial carefully.

Identify the Exact Reason for Denial

The reason matters. Different denial reasons require different responses.

For example:

| Denial Reason | Potential Response |

|---|---|

| No hail damage found | Obtain independent inspection |

| Damage attributed to age | Secure expert evaluation |

| Late filing | Gather reporting records |

| Excluded damage | Review policy language |

| Insufficient evidence | Collect additional documentation |

Understanding the insurer’s position helps determine your next move.

Compare the Denial to Your Policy

Insurance policies contain hundreds of pages. Most homeowners never read them until a problem occurs.

Now is the time.

Review:

- Coverage provisions

- Exclusions

- Endorsements

- Deductibles

- Claim reporting requirements

Pay attention to language the insurer cited in its denial.

Look for Errors

Mistakes happen.

Inspectors occasionally miss damage. Reports sometimes contain incorrect information.

Common examples include:

- Wrong roof age

- Incorrect storm dates

- Misidentified materials

- Missing damaged areas

- Incomplete inspections

Any inconsistency should be documented.

Step 2: Gather Additional Documentation

Strong documentation often determines whether a denial remains denied. Evidence matters. The more evidence available, the stronger your position becomes.

Photograph Everything

Take photographs immediately.

Capture:

- Roof damage

- Gutters

- Downspouts

- Siding

- Screens

- Exterior fixtures

- Interior water stains

Use multiple angles. Take wide shots and close-ups. Create date-stamped records whenever possible.

Collect Weather Documentation

Weather records can strengthen a disputed hail claim.

Useful sources include:

- National Weather Service reports

- Local weather stations

- Storm tracking data

- Radar imagery

- Hail size reports

These records help establish that a damaging storm occurred.

Obtain Previous Repair Records

Past maintenance records can be valuable.

Keep copies of:

- Roof inspections

- Previous repairs

- Contractor invoices

- Warranty documents

- Maintenance reports

These records may help counter claims that damage predated the storm.

Document Interior Damage

Roof damage often leads to interior problems.

Photograph:

- Ceiling stains

- Drywall damage

- Peeling paint

- Mold growth

- Flooring damage

Interior evidence can support the overall claim.

Keep a Communication Log

Create a simple tracking system.

Record:

| Date | Contact | Discussion |

|---|---|---|

| May 10 | Claims Adjuster | Initial inspection |

| May 18 | Insurance Representative | Denial discussion |

| May 25 | Roofing Contractor | Independent inspection |

This timeline may become important later.

Learn How to Document Hail Damage for an Insurance Claim

Many denied claims suffer from weak documentation. Homeowners who understand How to Document Hail Damage for an Insurance Claim typically present stronger evidence and create a clearer record of storm-related damage. The goal is building a complete file that demonstrates both the existence and extent of the loss.

Step 3: Request a Second Inspection

A surprising number of hail claim disputes stem from a single inspection. Think about that for a moment. One visit. One opinion. One report. That report may determine thousands of dollars in claim payments.

Why Initial Inspections Miss Damage

Several factors contribute:

- Time limitations

- Weather conditions

- Roof accessibility

- Inexperience

- Human error

No inspection process is perfect.

When a Reinspection Makes Sense

A second inspection may be appropriate when:

- Damage was overlooked

- New evidence becomes available

- Independent experts disagree

- Additional affected areas are discovered

The request should be professional and supported by documentation.

Participate in the Inspection

Whenever possible, attend. Take notes. Ask questions. Document observations. This ensures you understand how conclusions are reached and allows you to identify potential concerns immediately.

Step 4: Obtain an Independent Damage Assessment

This step often changes everything. Insurance companies rely on their own inspections. Homeowners should consider obtaining independent evaluations as well. An independent assessment provides a second perspective. Sometimes that perspective reveals significant damage that was previously overlooked.

Potential Sources of Independent Evaluations

These may include:

- Roofing contractors

- Building consultants

- Engineers

- Public adjusters

- Storm damage specialists

Each brings a different level of expertise.

What Independent Assessments Often Reveal

Independent reviews frequently uncover:

- Additional hail impacts

- Collateral damage

- Hidden roof deterioration

- Water intrusion pathways

- Damaged roofing components

The process can be surprisingly detailed. In some ways, it resembles a technical investigation. Much like researchers studying a complex system through the lens of phenomenology, damage evaluators often examine how multiple observations combine to reveal a broader picture that may not be obvious from a quick inspection. The key is obtaining a complete understanding of the property’s condition.

Step 5: Understand Your Rights Under Texas Insurance Law

Many homeowners feel powerless after a denial. They shouldn’t. Texas policyholders have important rights. Understanding those rights can significantly affect how a claim dispute unfolds.

Step 5: Understand Your Rights Under Texas Insurance Law

Many homeowners assume the insurance company has the final say. That isn’t always true. Texas law establishes standards for how insurers investigate, evaluate, and respond to claims. While every claim is different, policyholders are entitled to fair treatment throughout the process.

Insurers Must Conduct Reasonable Investigations

A denial should be based on facts. That means inspections, documentation reviews, and claim evaluations should be thorough and objective. If important areas were never inspected or significant evidence was overlooked, questions about the denial may arise.

Keep All Claim-Related Documents

At this stage, organization becomes critical.

Create a dedicated claim file containing:

- Insurance policy

- Denial letter

- Inspection reports

- Contractor estimates

- Photographs

- Emails

- Text messages

- Repair invoices

- Weather reports

The stronger your file, the stronger your position.

Time Matters

Do not place the denial letter in a drawer and forget about it. Many policies contain deadlines that may affect your ability to challenge the decision. The sooner action is taken, the better.

Step 6: File a Formal Appeal

Once additional evidence has been gathered, the next step is often a formal appeal. This is your opportunity to present information the insurer may not have considered during the initial review.

What Should an Appeal Include?

A strong appeal package may contain:

| Document | Purpose |

|---|---|

| Appeal Letter | Explains disagreement |

| Independent Inspection Report | Supports damage findings |

| Photographs | Visual evidence |

| Weather Data | Confirms storm event |

| Repair Estimates | Demonstrates financial impact |

| Supporting Documentation | Strengthens claim position |

Think of the appeal as telling the complete story. The goal is not to express frustration. The goal is to present evidence.

Write Clearly and Professionally

Avoid emotional language.

Instead:

- Focus on facts

- Reference documentation

- Cite inspection findings

- Explain discrepancies

- Request specific reconsideration

A professional presentation often receives more attention than an emotional response.

Common Appeal Mistakes

Homeowners sometimes hurt their own cases by:

- Submitting incomplete evidence

- Missing deadlines

- Providing unclear photographs

- Failing to address denial reasons

- Ignoring policy language

Each appeal should directly respond to the insurer’s stated reasons for denial.

Step 7: Consider the Appraisal Process

Many Texas homeowners have heard the word “appraisal” but are unsure what it means in an insurance dispute. Appraisal can be a useful tool under certain circumstances.

What Is Insurance Appraisal?

Appraisal is a dispute resolution process used when parties disagree about the amount of loss.

It typically involves:

- An appraiser selected by the policyholder

- An appraiser selected by the insurer

- An umpire who helps resolve disagreements

When Appraisal May Be Helpful

Appraisal is often considered when:

- Damage is acknowledged

- Coverage is not the primary issue

- The dispute involves repair costs

- Replacement scope is contested

When Appraisal May Not Be the Best Option

If the insurer completely denies that hail damage exists, appraisal may not fully resolve the dispute. Coverage issues frequently require different strategies. Understanding the difference is important before moving forward.

Step 8: File a Complaint With the Texas Department of Insurance

Sometimes homeowners believe the claim process itself was mishandled. In those situations, a complaint may be appropriate.

Situations That May Justify a Complaint

Examples include:

- Significant communication delays

- Failure to explain denial decisions

- Unreasonable claim handling concerns

- Lack of investigation

A complaint is not a guarantee that a denial will be reversed. However, it may encourage additional review.

Information You’ll Need

Prepare:

- Claim number

- Policy number

- Denial letter

- Supporting documentation

- Communication records

Organization matters. The easier it is to understand the issue, the easier it becomes for others to review it.

Step 9: How a Public Adjuster Can Help After a Denial

Many homeowners contact a public adjuster only after problems arise. In reality, denied claims are one of the most common reasons people seek assistance.

What Does a Public Adjuster Do?

A public adjuster works for the policyholder rather than the insurance company.

Their role often includes:

- Damage evaluation

- Documentation review

- Policy analysis

- Claim preparation

- Settlement negotiations

The objective is straightforward. Present the strongest possible claim supported by evidence.

Independent Damage Investigation

One major advantage is the ability to conduct an independent review.

This often includes:

- Roof inspections

- Exterior evaluations

- Interior assessments

- Documentation analysis

- Scope development

Additional damage is frequently identified during these reviews.

Negotiating With the Insurance Company

Negotiation requires preparation. Evidence drives results. A properly documented claim often creates opportunities for productive discussions that may not have existed previously.

Situations Where Public Adjusters Frequently Help

| Situation | Why Assistance May Help |

|---|---|

| Denied roof claim | Independent review |

| Underpaid claim | Scope analysis |

| Large property loss | Documentation support |

| Commercial property claim | Complex valuation |

| Multiple structures damaged | Comprehensive assessment |

For homeowners researching What to Do If Your Hail Claim Was Denied in Richardson, TX, professional representation is often one of the most effective ways to challenge an unfavorable decision.

Red Flags That May Indicate an Unfair Denial

Not every denial is improper. However, certain warning signs deserve attention.

Extremely Short Inspections

A roof inspection completed in just a few minutes may raise concerns. Thorough evaluations generally take time.

Missing Damage Areas

If obvious damage locations were never inspected, important evidence could have been missed.

Contradictory Findings

When multiple professionals reach dramatically different conclusions, additional investigation may be warranted.

Lack of Documentation

A denial supported by minimal evidence should be reviewed carefully. The stronger the insurer’s position, the more documentation typically exists to support it.

Mistakes Richardson Homeowners Should Avoid After a Denial

Receiving a denial creates stress. Unfortunately, stress sometimes leads to costly mistakes.

Mistake #1: Assuming the Denial Is Final

This is perhaps the most common mistake. Many denied claims are later reconsidered after additional evidence is presented.

Mistake #2: Throwing Away Evidence

Never discard:

- Damaged materials

- Inspection reports

- Estimates

- Photographs

- Claim correspondence

Even small pieces of evidence can become important.

Mistake #3: Delaying Action

Time rarely helps.

Waiting months to respond may complicate the process.

Mistake #4: Relying on Memory

Keep written records. Document conversations. Store emails. Maintain timelines. Memory fades. Documentation doesn’t.

Mistake #5: Accepting an Incomplete Investigation

If you believe important damage was missed, seek a second opinion. The cost of inaction can be significant.

Realistic Outcomes After Challenging a Denied Hail Claim

What happens after a denial is challenged? The answer varies. Every claim has unique facts. However, several outcomes are common.

Full Reversal

Sometimes additional evidence convinces the insurer to approve the claim.

Supplemental Payments

In other cases, additional funds are issued even if the original decision is not completely reversed.

Partial Approval

Certain damages may become covered while others remain disputed.

Appraisal Resolution

Appraisal occasionally resolves disagreements regarding repair costs.

Negotiated Settlement

Some disputes conclude through direct negotiations. The important takeaway? A denial does not automatically end the claim. For many Richardson homeowners, it represents the beginning of a deeper review process.

Why Professional Representation Often Changes the Outcome

Insurance claims involve more than photographs.

They involve:

- Policy language

- Damage analysis

- Documentation

- Construction knowledge

- Negotiation

That’s a lot for any homeowner to manage alone.

Experience Matters

Professionals understand:

- What evidence carries weight

- How damage is documented

- Which policy provisions apply

- How disputes are typically resolved

This experience often leads to stronger claim presentations.

Comprehensive Documentation Wins Claims

The strongest claims usually share one characteristic. Documentation. Not assumptions. Not opinions. Evidence. When evidence becomes organized, detailed, and persuasive, insurers often take a closer look. That reality explains why so many property owners seek assistance after receiving a denial.

What to Do If Your Hail Claim Was Denied in Richardson, TX: Final Thoughts

Receiving a denial letter can feel like a dead end. It rarely is. For homeowners searching for What to Do If Your Hail Claim Was Denied in Richardson, TX, the most important thing to remember is that options often remain available. Review the denial carefully.

Gather evidence. Request additional inspections. Seek independent evaluations. Understand your rights. Document everything. Act promptly. Most importantly, do not assume the first decision is necessarily the correct one. Hail claims are complex. Inspections vary. Evidence evolves. New information can emerge. Many denied claims ultimately look very different after a thorough review. For Richardson homeowners facing storm damage disputes, persistence, preparation, and strong documentation often make all the difference.

FAQs

Yes. Most homeowners can challenge a denial by providing additional evidence, documentation, or independent inspection reports.

It’s best to act as soon as possible because insurance policies may contain deadlines that affect your options.

An independent inspection may help determine whether the damage was caused by hail or normal aging.

Yes. A second inspection can uncover damage that may have been missed during the original evaluation.

Yes. Weather records can help verify that a hail-producing storm occurred near your property.

Keep the denial letter, policy documents, photos, inspection reports, estimates, and all claim-related communications.

A public adjuster can evaluate the damage, review the policy, and assist with documenting and negotiating the claim.

A denied claim receives no payment, while an underpaid claim provides compensation that may not fully cover the damage.

Yes. Some hail-related issues, including leaks and roofing deterioration, may not become obvious immediately after a storm.

No. Many denied claims are reconsidered when additional evidence or expert evaluations are submitted.